Energy Market Outlook: Heat, Supply, and Shifting Fundamentals

- Tony Zelinski

- 1 day ago

- 1 min read

As the U.S. enters peak summer demand, the energy complex is balancing strong production against surging consumption. The latest shows how weather, LNG exports, and regional power dynamics are shaping price behavior across commodities.

Natural Gas: Range‑Bound but Resilient

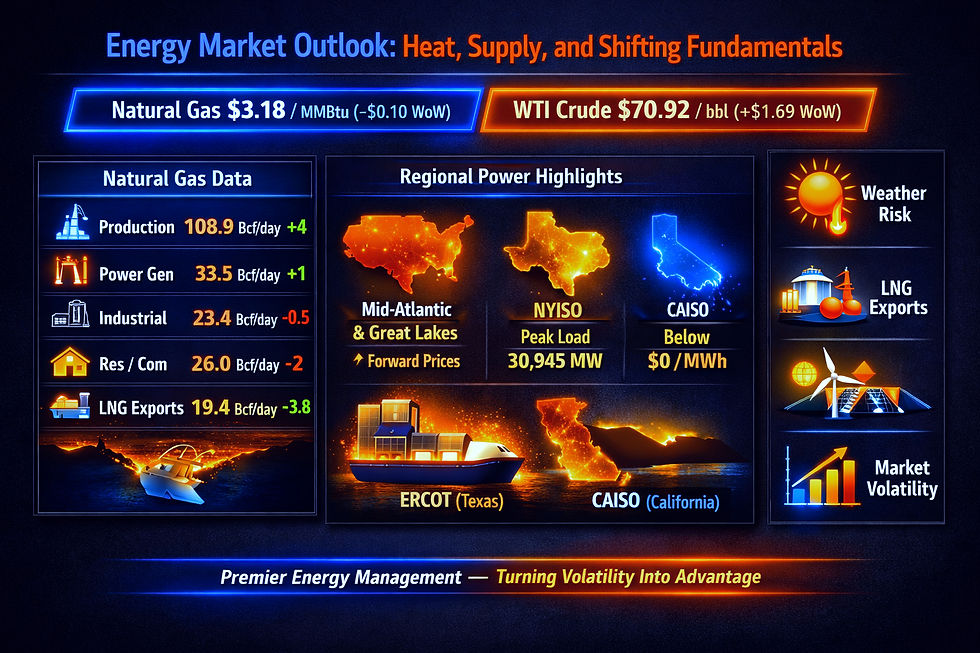

Prompt‑month natural gas settled at $3.18/MMBtu, down $0.10 from the prior week’s $3.25. Despite the dip, fundamentals remain neutral — supported by robust production and tempered by record power‑generation demand.

Metric | Current | Year‑Over‑Year Change |

Production | 108.9 Bcf/day | +4 Bcf/day |

Power Generation | 33.5 Bcf/day | +1 Bcf/day |

Industrial Consumption | 23.4 Bcf/day | –0.5 Bcf/day |

Residential/Commercial | 26 Bcf/day | –2 Bcf/day |

LNG Exports | 19.4 Bcf/day | +3.8 Bcf/day |

Inventories stand at 2,835 Bcf, 76 Bcf higher week‑over‑week, 49 Bcf below last year, and 152 Bcf above the five‑year average. The market remains range‑bound — capped by ample supply yet supported by summer cooling demand and export strength.

Crude Oil: Neutral to Bullish

WTI crude settled at $70.92/bbl, up $1.69 week‑over‑week. Geopolitical uncertainty in the Persian Gulf continues to drive volatility, with vessel traffic through the Strait of Hormuz at 53% of last year’s levels. Despite regional tension, Gulf producers maintain steady loadings, and U.S. sanctions waivers on Iranian oil remain in effect until August 21.

Power Markets: Regional Divergence

Mid‑Atlantic & Great Lakes: Forward power prices rose 1–2% week‑over‑week and 5% month‑over‑month as heat indices exceeded 100°F from Boston to Miami. Day‑ahead settlements reached $56.56/MWh in West Hub, 24% above May’s average.

Northeast: New York forward prices climbed 6% for Balance ’26 contracts, with

Cal ’29–’30 terms up 2–4%. NYISO forecasts peak load at 30,945 MW, approaching last summer’s

ICAP threshold.

ERCOT (Texas): System load exceeded 83 GW, peaking near 85 GW on June 29. Wind output averaged 16–23 GW and solar 11–13 GW, keeping real‑time prices near $25/MWh. Renewables set new records — combined output at 51,974 MW, wind at 28,928 MW, and battery charging at 7,847 MW.

Western Regions: Mild temperatures and strong renewables continue to pressure natural gas dispatch. CAISO day‑ahead prices briefly fell below $0/MWh amid oversupply, triggering

curtailments across solar and wind resources.

Economic and Weather Context

Gasoline Prices: Below $4/gallon for the first time in months.

Consumer Confidence: Up to 91.2 in June (from 90.6 in May).

Wholesale Inflation: 4.1% in May — a three‑year high.

Heat Wave: Extending through the July 4 weekend with indices above 100°F across the East

and Midwest.

Strategic Takeaways

Natural Gas: Expect continued range‑bound trading as production and storage offset seasonal demand.

Crude Oil: Geopolitical risk remains the wild card for price direction.

Power Markets: Regional heat and renewable penetration will drive short‑term volatility.

Risk Management: Dynamic hedging and weather‑linked analytics are essential for load forecasting and procurement strategy.

Premier Energy Management continues to help clients navigate these shifts — turning volatility into advantage through data‑driven insight and strategic market engagement.

#EnergyMarkets #NaturalGas #CrudeOil #ElectricityPrices #LNG #Renewables #ERCOT #NYISO #CAISO #MarketAnalysis #RiskManagement #PremierEnergyManagement #PEM #Volatility #EnergyStrategy #HeatWave #CommodityTrading #DataDrivenEnergy

Would you like a review of your facility's energy plan? We are here to help!

Comments