EIA Storage and Weather Balance Support Mid‑Summer Market Stability

- Tony Zelinski

- 12 minutes ago

- 2 min read

Monday, July 6 saw the front‑month NYMEX Natural Gas contract open at $3.182, up slightly from Thursday’s $3.196 close. After an early dip to $3.182 at 9:30 AM, prices climbed steadily through the morning, reaching an intraday high of $3.254 as traders weighed updated forecasts for late‑month cooling demand and waning production. By the afternoon, August futures closed higher at $3.245, signaling cautious optimism amid balanced fundamentals.

🔹 Storage and Supply Dynamics

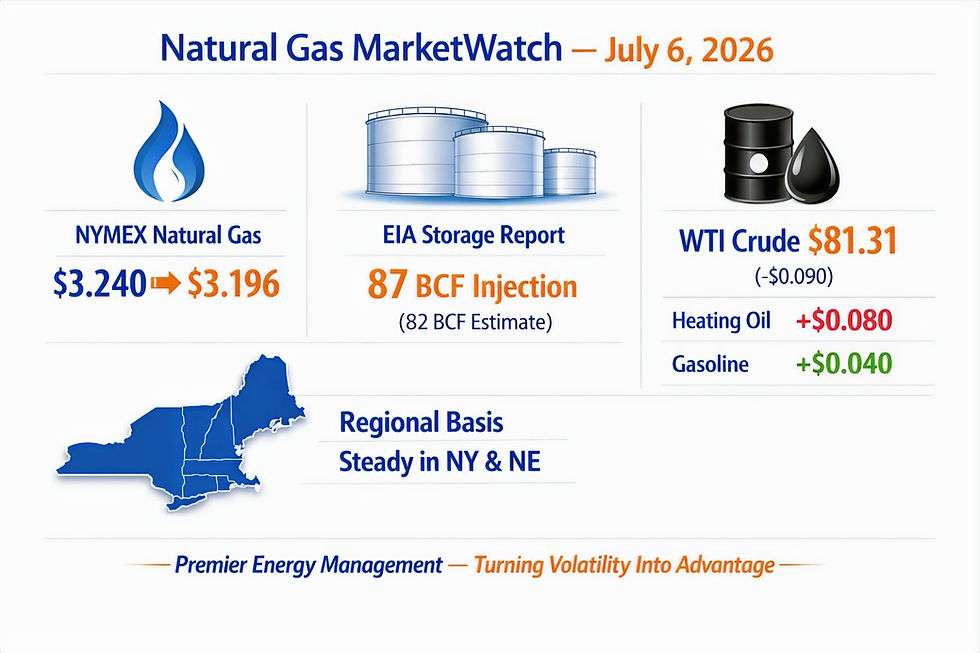

The EIA Natural Gas Storage Report released last Thursday posted an 87 BCF injection for the week ended June 26 — in line with the market estimate of 82 BCF. Working gas in storage now stands at 2,922 BCF, 0.8 % below last year and 6.4 % above the five‑year average.

This data confirms a market that remains well‑supplied heading into mid‑July, with inventories comfortably above seasonal norms.

🔹 Crude and Refined Products

In early Globex trading, WTI Crude rose $0.490 to $80.40, while Heating Oil slipped $0.039 and Gasoline fell $0.047. The mixed movement across refined products reflects divergent fundamentals — crude strength tied to geopolitical risk and refinery throughput, versus refined product softness driven by easing demand and inventory builds.

🔹 Regional Basis Trends

New York and New England basis values remain firm for the remaining summer months and early winter delivery, supported by localized demand and pipeline constraints. Cash prices were lower in both regions, but forward spreads continue to reflect structural tightness heading into the heating season.

🔹 Weather and Demand Outlook

Forecast models show above‑average temperatures across the South and Mid‑Atlantic, sustaining elevated cooling loads. Meanwhile, milder conditions in the Midwest and

Northeast temper overall demand. This regional balance keeps national consumption steady and supports a range‑bound price environment near the $3 support level.

🔹 Strategic Implications for Procurement

For commercial and industrial consumers, the current setup favors incremental hedging rather than aggressive forward locking. With storage builds steady and volatility subdued, short‑term procurement strategies can capitalize on dips while maintaining flexibility for late‑summer adjustments.

Longer‑term buyers should monitor basis spreads, regional weather patterns, and crude correlations, as these factors can quickly shift cost structures.

The interplay between storage injections, cooling demand, and macro energy trends will define price behavior through July.

🔹 PEM Perspective

At Premier Energy Management, we help clients interpret these signals — aligning procurement timing with market fundamentals to manage risk and capture opportunity. Our approach integrates real‑time data, regional basis analytics, and weather‑driven forecasting to ensure decisions are grounded in actionable insight.

As the summer unfolds, disciplined risk management and data‑driven strategy remain essential to navigating evolving supply‑demand dynamics. The market may be calm today, but volatility never stays dormant for long — and preparation is the best hedge.

#NaturalGas #EnergyMarkets #EIA #StorageReport #WTICrude #EnergyTrading #RiskManagement #PremierEnergyManagement #PEM #Volatility #EnergyStrategy #MarketWatch #GasPrices #EnergyInsights #Procurement #BasisRisk #WeatherForecasts #EnergyInfrastructure #CoolingDemand #GridReliability

Would you like a review of your facility's energy plan? We are here to help!

Comments