U.S. Natural Gas Storage Capacity Expands Slightly in 2025 — Regional Shifts Define the Trend

- Tony Zelinski

- 4 days ago

- 2 min read

Updated: 2 days ago

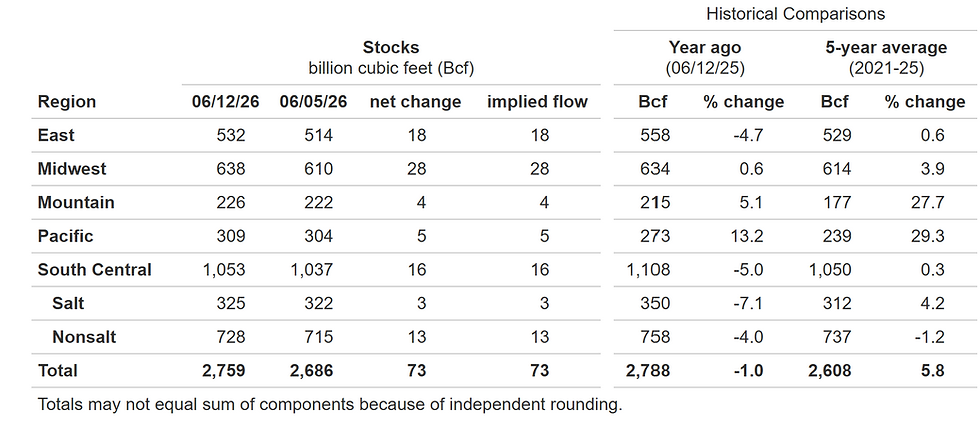

The U.S. Energy Information Administration’s latest Underground Natural Gas Working Storage Capacity Report shows that storage capacity in the Lower 48 states increased modestly in 2025, continuing a three‑year upward trend. While the overall gain was small — +0.1% or 6 Bcf — the regional story reveals how infrastructure investment and utilization patterns are evolving across the country.

📊 Key Data Highlights

Metric | 2024 → 2025 Change | Notes |

Demonstrated Peak Capacity | +6 Bcf (+0.1%) | Third consecutive annual increase |

Working Gas Design Capacity | +26 Bcf (+0.6%) | Total = 4,683 Bcf as of Nov 2025 |

South Central Region | +21 Bcf | Largest capacity addition nationwide |

Mountain Region | +6 Bcf | Continued expansion of storage sites |

Midwest Region | –5 Bcf | Decline linked to field utilization patterns |

Pacific Region | –8 Bcf | Reflects operational adjustments and base gas changes |

East Region | –15 Bcf | Reduced capacity from base gas reclassification |

⚙️ Understanding the Metrics

The EIA tracks two complementary measures of storage capacity:

Demonstrated Peak Capacity — the sum of the largest working‑gas volumes stored in each field over the past five years. It reflects actual usage rather than theoretical limits.

Working Gas Design Capacity — the certified maximum volume based on reservoir characteristics, equipment, and operating procedures.

Both metrics rose in 2025, signaling steady utilization of existing facilities and incremental additions of new facilities. The South Central and Mountain regions led the growth, while the East and Pacific regions saw minor declines due to base‑gas adjustments and operational changes.

🔍 Market Implications

Seasonal Flexibility Improves. Even small capacity gains enhance the system’s ability to balance supply and demand during peak winter draws and summer injections.

Regional Disparities Matter Growth in the South Central region — home to major salt‑dome storage — strengthens Gulf Coast market resilience and supports LNG export flows.

Infrastructure Optimization Continues. The modest national increase reflects a mature market focusing on efficiency rather than large‑scale expansion.

Policy and Investment Signals. Incremental capacity growth suggests regulatory

stability and ongoing investment in storage modernization to support grid reliability and

energy security.

💡 PEM Perspective

At Premier Energy Management, we view the 2025 storage data as evidence of a steady, disciplined market — one that’s optimizing infrastructure rather than chasing volume. For clients, this means:

Reliable seasonal balancing across regions

Predictable basis behavior tied to storage availability

Opportunities for strategic hedging as regional capacity shifts affect price differentials

Storage remains the quiet backbone of U.S. energy resilience — a system that ensures supply stability even as production and exports fluctuate.

#NaturalGas #EnergyMarkets #EIA #StorageCapacity #Infrastructure #EnergySecurity #SouthCentralRegion #MountainRegion #BasisMarkets #RiskManagement #PEM #MarketAnalysis #EnergyStrategy #USEnergy #GasStorage #EnergyInsights

Would you like a review of your facility's energy plan? We are here to help!

Comments