📉 EIA Natural Gas Storage Report – Week Ending March 6, 2026

- Tony Zelinski

- Mar 12

- 2 min read

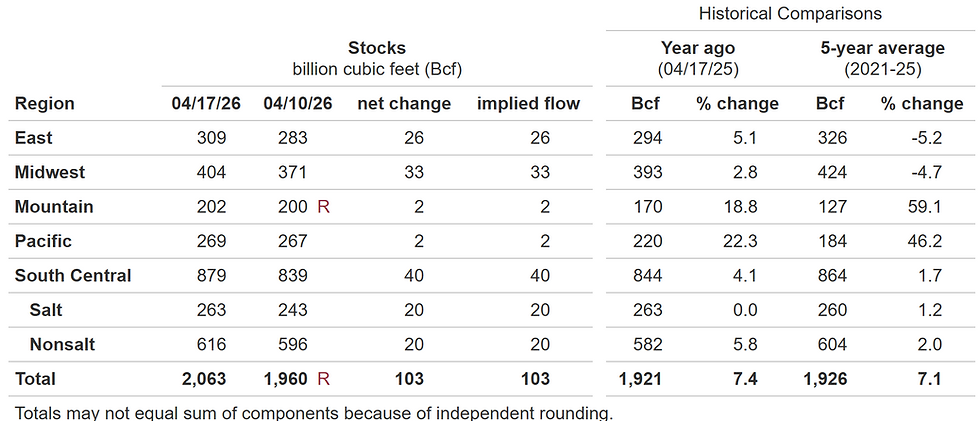

The latest EIA Weekly Natural Gas Storage Report for the week ending March 6, 2026, delivered a measured but meaningful update for market watchers. Working gas in storage fell 38 Bcf, bringing total inventories to 1,848 Bcf—a level that sits 141 Bcf above last year but 17 Bcf below the five‑year average. Despite the week‑over‑week draw, stocks remain comfortably within the five‑year historical range.

Regional Shifts: A Mixed but Balanced Picture

Storage movements varied across regions, reflecting localized weather patterns and demand dynamics:

East: –28 Bcf, the largest regional draw, consistent with lingering late‑season heating demand.

Midwest: –22 Bcf, another notable pull as temperatures fluctuated across the region.

Mountain & Pacific: Both regions posted small injections (+2 Bcf each), continuing their trend of elevated year‑over‑year surpluses.

South Central: A net +9 Bcf, driven by an 8 Bcf salt injection and flat nonsalt activity.

The South Central region remains the most structurally important for shoulder‑season balance, and this week’s injection underscores the ongoing flexibility in salt storage operations.

How Today’s Report Fits the Broader Market Narrative

With inventories still above last year but slightly below the five‑year norm, the market continues to navigate a tug‑of‑war between robust production and variable weather-driven demand. The modest draw aligns with expectations for a mild late winter, and the overall storage position suggests the market is entering the spring shoulder period with adequate but not excessive supply.

For traders, the report offers no major surprises—but it does reinforce the importance of watching regional flows, especially in the South Central, where salt storage behavior often telegraphs near‑term market sentiment.

Key Takeaways for Market Participants

Inventories remain healthy, reducing near‑term supply risk.

Regional divergence—notably the East draw vs. South Central injection—highlights shifting demand patterns.

Year‑over‑year surplus persists, but the slight deficit vs. the five‑year average keeps the market from feeling oversupplied.

Shoulder season dynamics will increasingly shape price action as weather-driven demand tapers.

#NaturalGas #EIA #GasStorage #EnergyMarkets #Commodities #WinterOutlook #HenryHub #LNG #WeatherRisk #NatGas

Sources:

Natural Gas Futures

Read more: EIA

When was the last time you reviewed your facility's Energy plan?

What are you waiting for?

We are here to help...

Comments