📉EIA Natural Gas Storage Report – Week Ending April 17, 2026

- Tony Zelinski

- Apr 23

- 2 min read

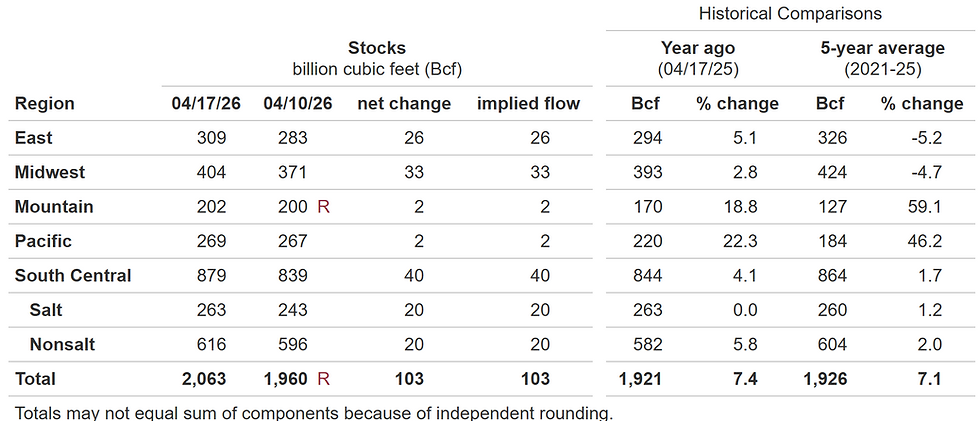

U.S. natural gas inventories rose sharply last week, underscoring a comfortable supply outlook as mild spring weather continues to limit demand. The EIA reported an injection of 103 Bcf into underground storage for the week ending April 17, vs. an estimated injection of 92 Bcf. A reported revision caused the stocks for April 10, 2026, to change from 1,970 Bcf to 1,960 Bcf. As a result, the implied net change between the weeks ending April 03 and April 10 changed from 59 Bcf to 60 Bcf.

63 Bcf, 142 Bcf, or 7.4% more than the same period last year, and 137 Bcf or 7.1% more/less than the 5-year average.

A variable pattern that allows warmth across the southern tier will push into the Midwest over the next several days, though the East Coast may struggle to warm. The pattern looks more amplified as we head into the first weekend of May, which should bring chilly conditions to the eastern half of the nation, with the West trending milder/warmer.

U.S. power and natural gas prices continue to be driven by typical shoulder season factors, with limited heating or cooling demand to move the meter one way or the other.

Yesterday, oil prices rose, as Iran claimed to have seized two ships in the Strait of Hormuz shortly after Trump extended the ceasefire.

Key Data

Total working gas: 2,063 Bcf

Weekly change: +103 Bcf

Year‑over‑year: +142 Bcf

Versus 5‑year average: +137 Bcf

Regional highlights:

South Central: +40 Bcf (Salt +20 Bcf | Nonsalt +20 Bcf)

Midwest: +33 Bcf

East: +26 Bcf

Pacific: +2 Bcf

Mountain: +2 Bcf

At 2,063 Bcf, storage remains within the five‑year historical range, signaling balanced fundamentals despite steady production near 109 Bcf/d and LNG feedgas flows around 18.8 Bcf/d.

Market Context

Front‑month NYMEX NG1! futures fell 3.8% to $2.61/MMBtu following the release, reflecting trader expectations that ample inventories will temper near‑term price recovery. Global benchmarks remain elevated — TTF $14.60/MMBtu and JKM $15.81/MMBtu — driven by geopolitical risk premiums and Asian procurement ahead of summer cooling demand.

Analyst Takeaway

The EIA’s 103 Bcf build reinforces a theme of structural oversupply entering Q2. While production efficiency and LNG exports sustain long‑term bullish potential, near‑term sentiment is dominated by weather and storage metrics.For energy managers, this environment favors disciplined hedging and data‑driven procurement strategies to navigate volatility.

PEM Perspective

At Premier Energy Management, we view this week’s report as a reminder that volatility is data‑driven — discipline defines resilience. Our focus remains on translating market signals into actionable insights for clients managing exposure across gas, power, and renewables.

#NaturalGas #EnergyMarkets #EIA #StorageReport #CommodityTrading #EnergyInsights #RiskManagement #MarketUpdate

Sources:

Natural Gas Futures

Read more: EIA

When was the last time you reviewed your facility's Energy plan?

What are you waiting for?

We are here to help...

Comments