📉 EIA Natural Gas Storage Report – Week Ending June 5, 2026

- Tony Zelinski

- 6 days ago

- 2 min read

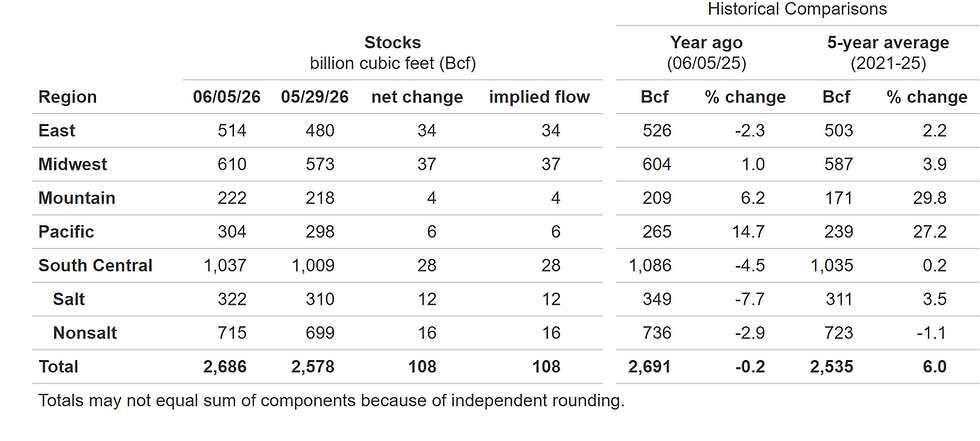

The U.S. Energy Information Administration (EIA) reported a 108 Bcf injection into underground storage for the week ending June 5, 2026, bringing total working gas to 2,686 Bcf .

This marks a steady but seasonally moderate build, reflecting the early onset of cooling demand across the Lower 48 states.

📊 Regional Breakdown

Region | Week‑over‑Week Change (Bcf) | Stocks (Bcf) | % Change vs Last Year | % Change vs 5‑Year Avg |

East | +34 | 514 | −2.3 % | +2.2 % |

Midwest | +37 | 610 | +1.0 % | +3.9 % |

Mountain | +4 | 222 | +6.2 % | +29.8 % |

Pacific | +6 | 304 | +14.7 % | +27.2 % |

South Central | +28 | 1,037 | −4.5 % | +0.2 % |

Total | +108 | 2,686 | −0.2 % | +6.0 % |

The Mountain and Pacific regions continue to post the largest year‑over‑year gains, underscoring the rebound in western inventories after last year’s drawdowns. By contrast, South Central salt storage fell 7.7 % from 2025 levels, suggesting tighter flexibility for peak‑season balancing.

⚙️ Market Context

With total stocks 151 Bcf above the five‑year average, the market remains comfortably supplied — yet traders are watching weather‑driven demand closely. Forecasts for above‑normal temperatures across the Midwest and East through mid‑June are expected to lift power‑sector gas burn, potentially slowing injections later this month.

At the same time, production near 109 Bcf/day and strong LNG flows (~18.6 Bcf/day) continue to anchor supply fundamentals. The balance between record output and rising cooling demand will determine whether storage levels stay within the historical range or begin to tighten heading into July.

🌡️ Strategic Takeaways for Energy Managers

Monitor regional basis spreads — particularly in the South Central salt facilities, where flexibility is narrowing.

Watch weather models — sustained heat could shift injections below the five‑year trend by late June.

Evaluate LNG export exposure — global supply disruptions (Qatar, Hormuz) may sustain U.S. export premiums.

Plan procurement windows — moderate builds now could precede sharper price moves if cooling demand accelerates.

🧭 PEM Perspective

At Premier Energy Management, we interpret weekly EIA data not just as numbers but as signals — guiding clients through hedging, procurement, and risk‑management decisions that anticipate volatility rather than react to it.

The current storage trajectory suggests a stable but tightening market, where fundamentals — weather, production, and exports — will drive direction through the summer.

#NaturalGas #EIAStorage #EnergyMarkets #RiskManagement #PremierEnergyManagement #Commodities #LNG #EnergyStrategy #MarketUpdate #GasPrices #Procurement #Hedging #EnergyInsights #Utilities #HedgingStrategy

Sources:

Natural Gas Futures

Read more: EIA

When was the last time you reviewed your facility's Energy plan?

What are you waiting for?

We are here to help...

Comments